-

Software

iPoint Suite

Digitalize your product life cycles on your journey from compliance to sustainability

ComplianceSecure your products & your business

SustainabilityFuture-proof your products & ideas

The EU Non-Financial Reporting Directive – An Introduction

The EU Non-Financial Reporting Directive (NFRD) 2014/95/EU was adopted by the EU in 2014. With this new legislation, public-interest entities in EU member states no longer only report on their financial basics and forward-looking risk discussion. They now also retrospectively account for their non-financial footprint, including adverse impacts they have on the environment and society.

The Directive applies to the current member states of the EU and was required to be transposed into the latter’s national laws by December 6, 2016, with companies obliged to provide enhanced disclosure from 2017 onwards. Considering the history of the CSR concept, one observer noted that what was once a voluntary format is now a legal requirement in the present Directive 2014/95/EU.*

Article 1 of the Directive states that the non-financial disclosure must contain information including: “e. non-financial key performance indicators relevant to the particular business”** – a point of departure for the following studies.

* Andorfer: Symbol- oder Impulspolitik. Das Transparenzkonzept, ein mittelbares Instrument der Politik zur Forcierung einer ressourcenorientierten Unternehmensausrichtung. Eine konzeptionelle Betrachtungsweise am Beispiel der Richtlinie 2014/95/EU, Berlin 2018, p. 141.

** Official Journal of the European Union, Directive 2014/95/EU of the European Parliament and of the Council of 22 October 2014, L 330/1, November 15, 2014, eur-lex.europa.eu/legal-content/EN/TXT/PDF/

The Reports

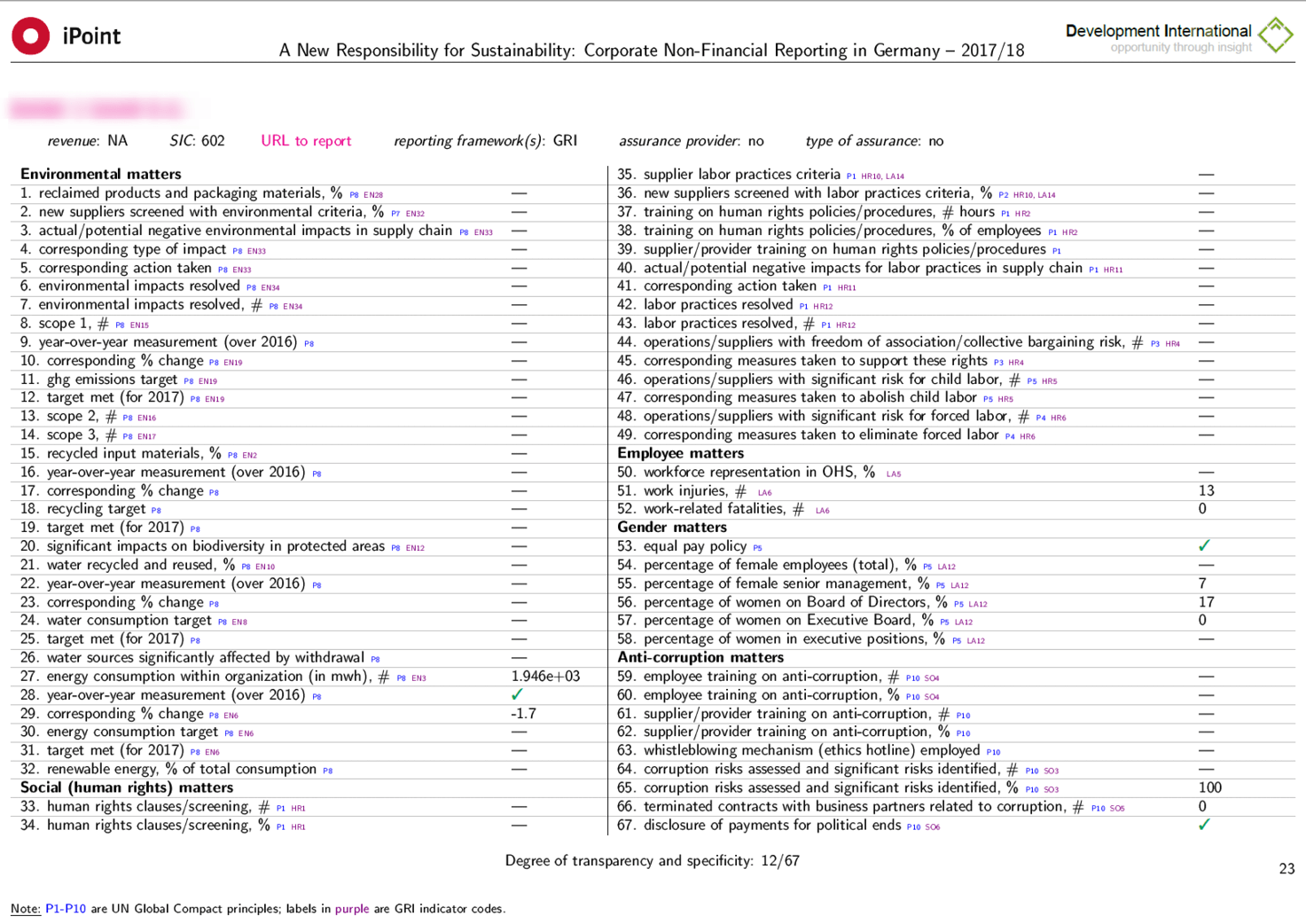

In 2019, not-for-profit organization Development International released the first set of comprehensive baseline studies which systematically assess the degree of non-financial transparency and ESG (environmental, social, and governance) performance for 2017 in Germany, Sweden, and Austria. The comprehensive studies – to date the only ones to focus on ESG performance in non-financial corporate reports – apply an ex-post assessment framework premised on 60+ key performance indicators based on the reporting frameworks of the Global Reporting Initiative (GRI), the German Sustainability Codex (DNK), and UN Global Compact.

This deep-dive into the five required disclosure areas – environmental, social and employee matters, respect for human rights, as well as anti-corruption and bribery matters – reveals the degree to which companies make an effort to demonstrate their environmental and social responsibility.

The country-specific studies assess 516 German, 590 Swedish, and 89 Austrian companies, and issue individual scorecards for them each. The reports for Germany, Sweden, and Austria can be downloaded below.

Report Germany

Report Sweden

Report Austria

Webinar Germany

Your speakers:

Dr. Chris N. Bayer, Development International e.V.

Dr. Katie Boehme, iPoint-systems gmbh

Matthias Keitel, iPoint-systems gmbh

Language:

German & English

Duration:

1 hour (including Q&A period)

Date:

May 23, 2019

Webinar Sweden

Your speakers:

Dr. Chris N. Bayer, Development International e.V.

Dr. Katie Boehme, iPoint-systems gmbh

Matthias Keitel, iPoint-systems gmbh

Language:

English

Duration:

1 hour (including Q&A period)

Date:

May 23, 2019

Webinar Austria

Your speakers:

Prof. Dr. Rupert Baumgartner, Institute for Systems Sciences, Innovation and Sustainability Research at the University of Graz

Dr. Chris N. Bayer, Development International e.V.

Language:

German & English

Duration:

1 hour (including Q&A period)

Date:

November 27, 2019

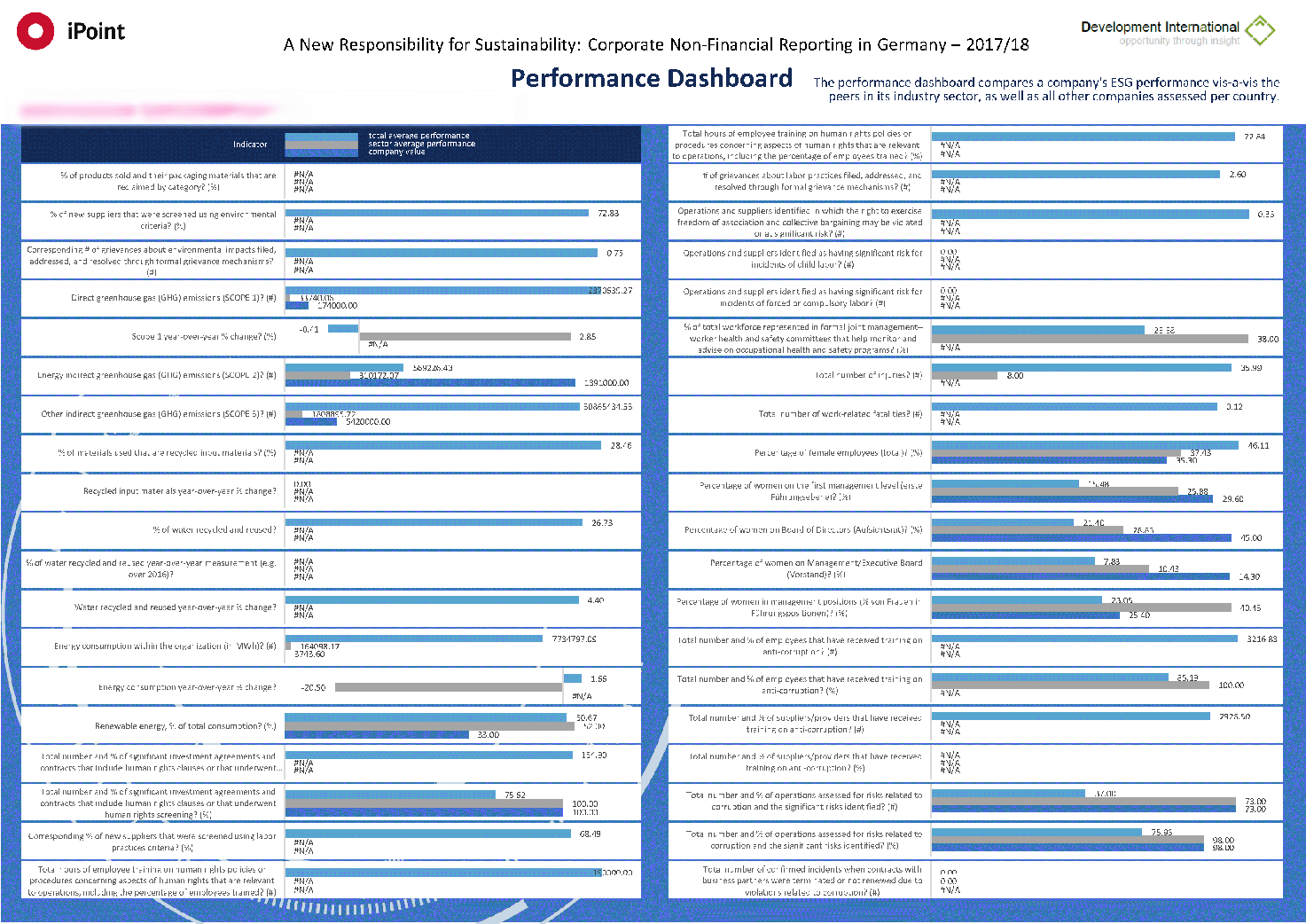

Corporate ESG Snapshot: Performance Dashboard & Transparency Scorecard

For each evaluated company, a Corporate ESG Snapshot has been created, showing how the evaluated companies scored on non-financial key performance indicators. Each Corporate ESG Snapshot delivers insights in to two different dimensions:

Transparency scorecard

The transparency scorecard accounts for the presence or absence of a particular data point, and tallies up how many featured KPIs a company employed.

Performance dashboard

The performance dashboard compares a company's ESG performance vis-a-vis the peers in its industry sector, as well as all other companies assessed per country.

Has my company been evaluated?

Check the list of evaluated brands:

Take a look at our other studies

This study assesses the 134 confirmed in-scope French corporations under the Devoir de Vigilinace…

The first comprehensive benchmarking report evaluated 1,504 brands on their anti-slavery disclosure…